Sansera Engineering

Pivoting from Pistons to Air-planes and clean rooms: How Sansera is Engineering Its Future in Aerospace, Defence and Semicon

Sansera Engineering Limited is a precision engineering company that designs and manufactures complex, mission-critical components for some of the world’s leading automotive, aerospace, defence and industrial OEMs. The company specializes in critical forged and machined components for automotive and non automotive customers. While historically known for producing components like connecting rods, rocker arms, and crankshafts for internal combustion engines, the company is now aggressively diversifying into high-growth sectors such as electric vehicles (xEV), aerospace, defence, and semiconductor equipment. From machined aluminum parts for EV drivetrains to Class 1000 clean-room assemblies for aerospace and semiconductor applications, Sansera is quietly becoming a key player in the global precision manufacturing value chain.

Before we go ahead, I want to give shout-out to Portseido whose product I just love 😃

Portseido helps in tracking investments in both Indian stocks and global stocks. It lets you create multiple portfolios and see performance by each portfolio as well as all combined. It connects with Indian brokers and global brokers such as IBKR and several others and also gives option to sync investments located in a google sheets.

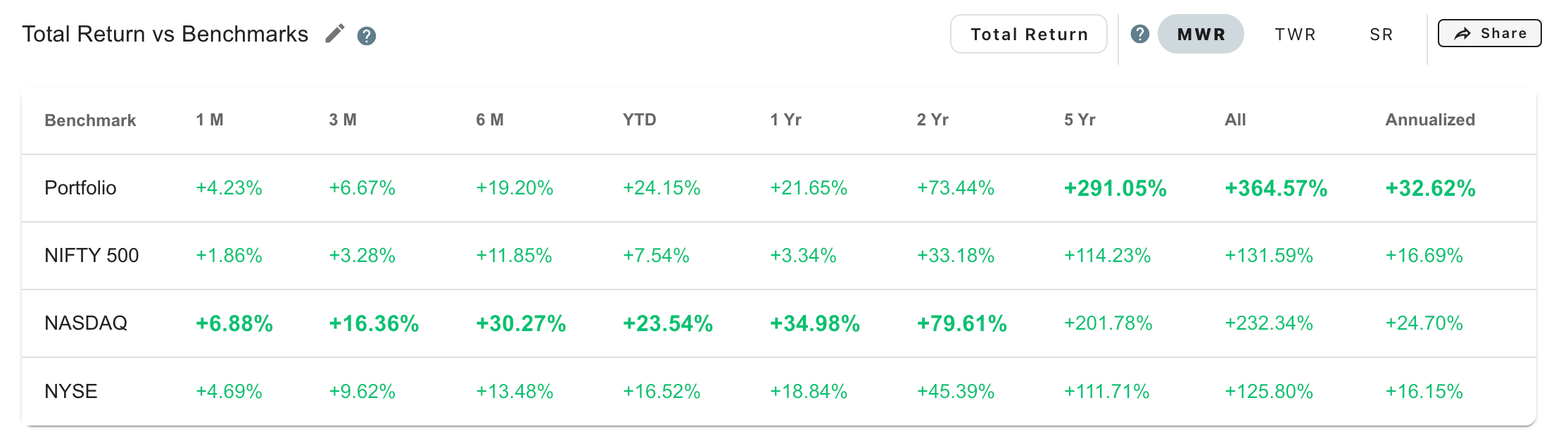

What I like about Portseido is we can see IRR returns in three ways - MWR (Money-weighted IRR), TWR (Time weighted IRR), SR (Simple IRR)

I really like this view to know where my PF is standing 😀 (PS: This is just descriptive table and not my real returns view)

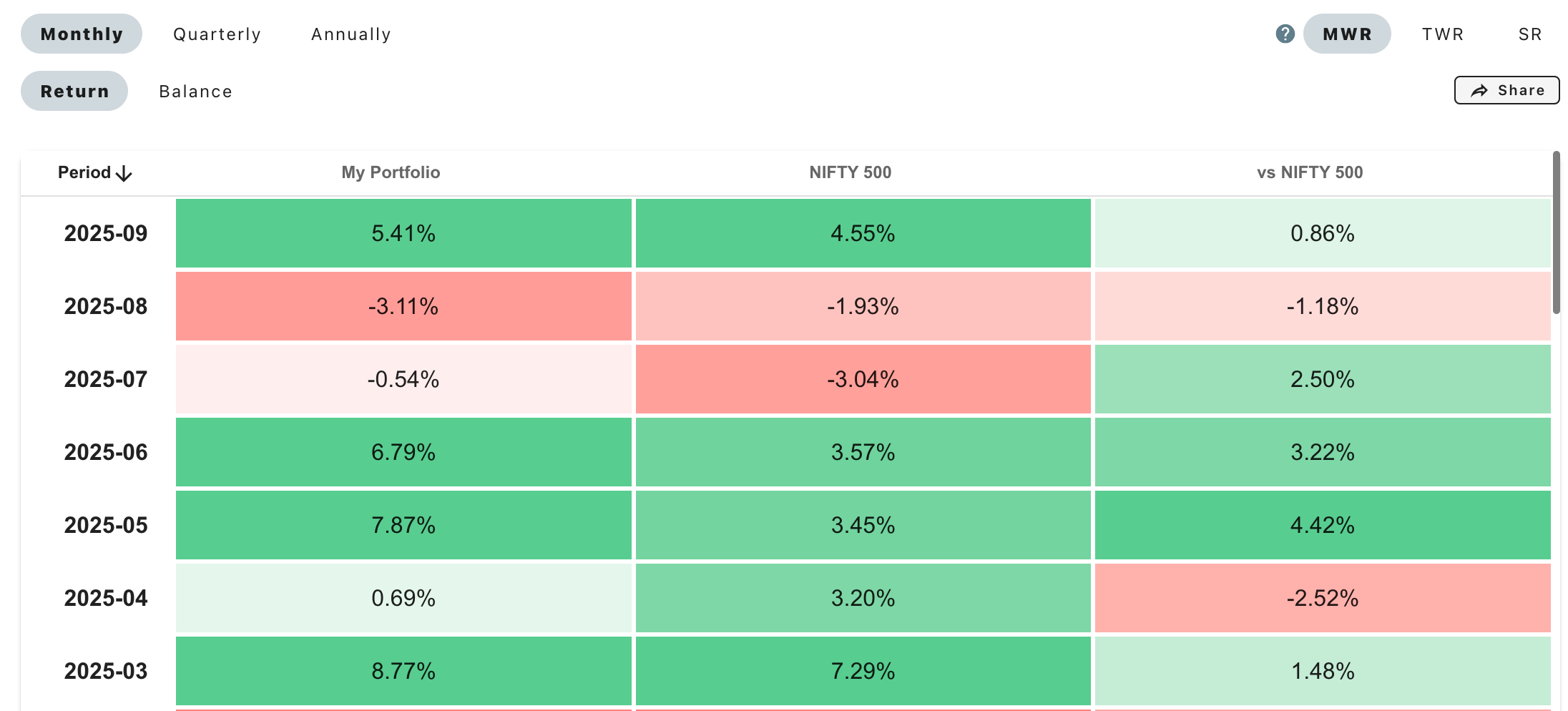

One can also see returns by each month and by each year in this view

You can signup for free trial at Portseido and track all your Global and Indian investments in one place at - Portseido.

Lets come back to discuss Sansera.

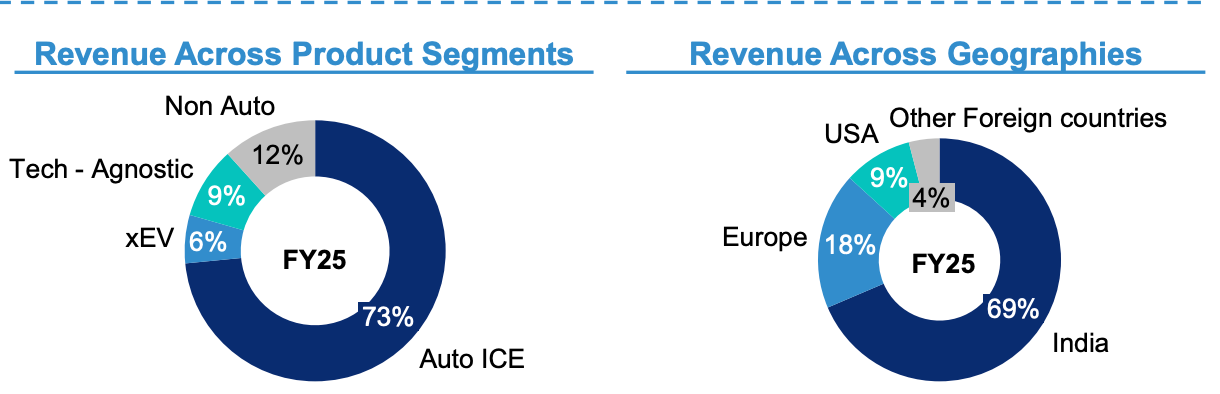

Revenue segmentation

Sansera is largely an Auto-ICE player today where it supplies parts such as …

It is trying to expand its non-ICE auto business and non auto business segments which are 27% of the business today

Non auto business segment is most interesting as this is the division where they are making precision components for aerospace, defence and semiconductor usecases

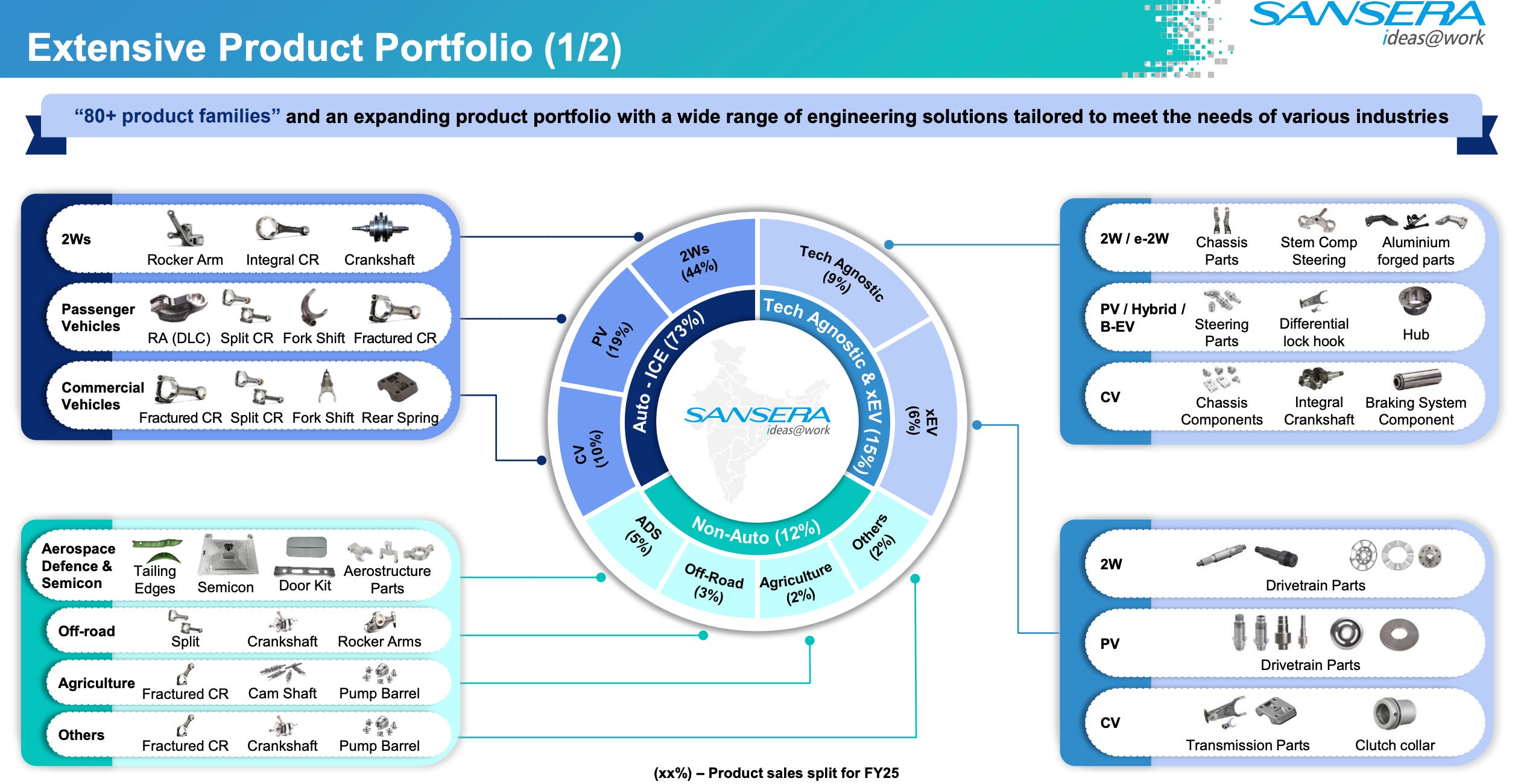

Product Portfolio & End User Segmentation

Sansera majorly caters to motorcycles in its 2-W business and this segment is 36% of overall revenues of FY25, rest 8% is 2-W scooters

PV business is only 19% as of FY25

Aerospace is 4-5% of overall FY25 revenue while defence and semiconductor businesses were negligible in FY25

Some key products in ADS segment

We would focus specifically on ADS (Aerospace, defence and semiconductor segment) in the blog as this is going to be major driver of Sansera’s growth and margins going forward and de-risks the business from the cylicality of the auto industry.

Lets look at some of the different aerospace and defence parts Sansera is manufacturing -

Engine casing

An engine casing is like the outer shell or protective skeleton of an engine.

If the casing fails, the engine can explode or stop working.

It's a precision product that must be leak-proof, heat-resistant, and strong under stress.

Engine Manufacturers (Rolls Royce, GE Aviation, Pratt & Whitney) are buyers of such product

All these players have growth outlook of mid to high single digits for next 5-6 years, which implies players like Sansera can grow in double digits as they have very big TAM to grab market share from in these kind of products

Trailing Edges

The trailing edge is the thin rear part of the wing, tail, or control surface (like flaps and rudders) where the air exits after flowing over the wing.

Buyers (aircraft OEMs and tier-1 integrators):

Airbus – for A320, A350, A220, etc.

Boeing – for 737, 777, 787

Dassault, Embraer, Lockheed Martin, Northrop Grumman

HAL and DRDO in India – for LCA Tejas, trainer aircraft

Door kits

Manufacturing door kits for aircraft is a high-precision, multidisciplinary task that demands capabilities across design, materials, machining, systems integration, and certification

Advanced Materials Expertise: Knowledge of aerospace-grade alloys and composites; forming and treating them to precise specs.

High-Precision Machining: 5-axis CNC, sheet metal work, tight-tolerance fabrication.

All the above products need to be certified and go through rigorous testing process as these are critical components in aerospace and defence and any shortcomings in such products can lead to safety issues

Some of the customers that Sansera has in ADS segment -

Airbus

Boeing

Saab

Triumph Aerospace

Management Commentary

Let us now study the management commentary on different segments of the business to understand the growth drivers better.

Strong commentary on ADS business for FY26 as management has guided for this business to double in FY26 (300 Cr revenue from ADS business is expected in FY26)

Management: Arjun, going forward, you will see a bigger number there. Just to add to what Vikas said that while we have renamed it as ADS, the meaningful ADS contribution will happen this year because a lot of qualification on the semicon and defense has happened now and we are now just starting the mass production of the semiconductor piece because these are -- I would say these are, for us, at least at Sansera, these were totally different technology altogether, much higher level of precision and kind of operations that we are doing, especially in semicon area. And with this added, we expect that as I've told in my commentary also that we expect the ADS business to be on a safer side, should deliver double the revenue of last year. We expect that it would be more than that. But then given a lot of pieces, puzzles which needs to be put together, I would still say that doubling the revenue is definitely on target because that is -- keeping that in mind, we have also done a lot of investment, both in terms of machining facility, in terms of - Level 1000 clean room, quality systems and also special processes.

Boeing and Airbus both seem to be customers of Sansera

Management: The underproduction of aircrafts in recent years has resulted in a very large order backlog, and with the ending of strike at Boeing, we expect the business to be back on the expected growth trajectory. We have entered into a strategic MOU with Dynamatic Technologies, allowing us to leverage our manufacturing and engineering expertise in producing high-friction parts going into the Airbus A220 aircraft door assemblies.

Management is confident about semiconductor business going forward

Gaurav Gandhi: Just 1 question, sir. This order regarding semiconductor equipment you are talking about, will this order be recurring in nature or onetime? And is there any more better opportunity in this space for the company?

Management: Yes. This is definitely a recurring order, and we expect that once we -- you start establishing yourself in any sector, you would have definitely higher opportunity, both with the same customer as well as with a few more of these players who are dominant in this industry. We are creating certain kind of facilities, which are very, very typical for this sector, including Class 1,000 clean room, also with some of the very high-end capability of machining. All these things should definitely aid us to improve our standing in the sector.

Management is optimistic on PV business despite its decline of about 7% in FY25

Actually, our order book has been very strong from the PV segment. In fact, we expect to outgrow our performance in the coming year as well as years to come. Overall, if you really look at our average growth, this segment will grow faster for us because there are several opportunities where we have already contracted further new orders from the -- both from North America, Latin America as well as India OEMs exports and Indian domestic segment.

Management is expecting stronger growth in Auto-tech agnostic & xEV business

Backdrop -

Tech-Agnostic Business

Softness in growth was acknowledged due to:

Insolvency of a European premium OEM.

Slower-than-expected pickup in premium domestic vehicle models.

xEV Segment

Entered a stabilization phase in FY25, focusing on:

Operational consolidation.

Cost structure understanding.

Margin profile improvement after clearing the learning curve on high-grade (Class A) aluminum components

In summary Sansera has slowed down the order book in this segment to focus on the margins more and execute the business efficiently

Management: In fact, like last time, I had told that we have had enough order book to focus on consolidation of our operations to improve the margin profile, improve the operational efficiency. That is the phase in which we are working, especially on aluminum forged and machine components because we have a very healthy order book totally about -- totaling about -- close to be about INR400 crores totally. And this year, our focus will be to execute it in a more efficient manner, where most of the learning curve has already passed us. We have gone through all the learning curves, especially on Class A components where a lot of product learning and technology learning went through. And we are quite confident now that this year, it would be returning a stronger growth.

The kit value of tech agnostic components in motorcycles is 4-5x of ICE components that are being used currently

Management: We have spoken about the kit value consistently over the period. So depending upon what kind of model that we work with, if it is -- see Tech Agnostic components generally are all aluminum forge and machine components. So in the scooter segment, there are limited number of such components which are there. It could be suspension, it could be some in braking, some in suspension. So there would be -- if you really look at as ICE scooter versus EV scooter, the content per vehicle for us largely remains the same, but the addressable market would between INR4,000 to INR5,000 per vehicle. But whereas if you really look at once the shift of electric vehicles happens towards motorcycles, then that is where the real game changer will be because that is where the content per vehicle is expected to go up significantly because the lightweighting requirement on the motorcycles is far higher than the requirement in the so -. So just to put a figure that if we are able to secure all the components that we are doing for similar models, it could go up to a 5-digit mark, could go up to almost INR10,000 per vehicle as the kit content. So this is how contextually you'll have to see, vis-a-vis about an average ICE motorcycle content of between INR1,800 to INR2,000, that's where we are.

Sansera has 30% stake in MMRFIC which was involved in radar systems used for Operation Sindoor

Management: To be very clear, MMRFIC today, given the context at which we are today currently post the operations Sindoor where you have seen a lot of technology that was used. This company is specifically in the midst of developing technologies for all those things what we saw, be it on speaker radars for very accurate striking missiles or EW radar system, or loitering ammunitions or for that matter, the border surveillance. The company is working very, very closely with various developmental projects, which are -- some of them are in the testing phases and these would be very, very strategic in terms of the technology that India is trying to indigenize. Currently all these technologies, as I previously mentioned, were also being -- are also being imported, and there is a lot of emphasis from the government side to indigenize these technologies.

Overall management is guiding for double digit growth in auto business to come back

See, as we said that our progress towards achieving 40% on Auto, Tech Agnostic, xEV and Nonauto business and we are well placed to go into that. And if you really look at how we are looking at -- aero, I already told that we are looking at doubling the this thing, it is more than 100%. We expect that two-wheelers should grow between 10% and 12%. This is for us. This is for Sansera's revenue growth. We expect Passenger Vehicle segment to grow between 15% to 17%. And Commercial Vehicle will also do a double-digit growth. This is broadly what I can say.

Thesis

Strong guidance

Guidance of high teens CAGR growth. Management specifically said they would get back to 18%-19% growth delivered in last 4 years. They expect to cross 5000 Cr revenue around FY28

Margin Improvement

Margin improvement outlook by 50-60 bps year over year as product mix shifts to ADS and EV business

Deleveraging

Management had indicated debt reduction by 700 Cr using the QIP money. They said that this would reduce the interest cost by 55 Cr per annum. This would reduce the interest cost by 55 Cr. As of FY25, ~500 Cr debt has been reduced, so it would be worth tracking further debt reduction here

ADS segment at inflection point

Sansera has spent last 2-3 years getting several approvals in aerospace, defence and semiconductor segments and FY26 could be the inflection point year if they double the ADS revenue to around 300 Cr. In FY27 as well, strong growth could come in the ADS segment as they have ~600 Cr order book which would take 2-3 years to exceute

Tailwinds in auto business

As Auto ICE business moves to more xEV side, the kit value of the Sansera's products could increase as they indicated in case of motorcycles which is their main segment in auto has almost 4-5x kit value.

Sansera has customers like Bajaj, Royal Enfield, Hero in domestic 2-W market and if 2-W demand remains buoyant, then along with premiumization, this segment could support overall growth.

Anti-Thesis

Demand problems and weakness in exports: Weak demand in automotive sector in EU & US which are major markets for Sansera

Customer Concentration Risk: Although improving, the top 5 customers still contribute ~46% of total revenue (FY25), down from 47.3% in FY24

Geopolitical events and tariffs: Adverse geopolitical events, tariffs, or regulatory shifts (e.g., EU emission standards) could disrupt operations.

Execution Risk: Sansera is scaling aggressively into Aerospace, Defence, and Semiconductors (ADS).

These require complex qualifications, long gestation periods, and tight tolerances.

Any delay in order ramp up, cost overruns, quality issues could impact margins and credibility

Tech-Agnostic & xEV Stabilization Risk: Management noted short-term softness and slower order intake in Tech-Agnostic and xEV segments. If this business remains soft it could also slower the overall growth and impact margins

Raw materials risks:

Forex fluctuations, rising aluminum/steel input costs, or supply disruptions can affect margin stability.

Sweden subsidiary associated risk: Sansera has a subidiary in Sweden which is 5-6% EBITDA margin business. Usually European subsidiaries struggle in margins as cost structures of these countries are significantly high. Any more pressure here can cause some problem in overall margins

Valuations

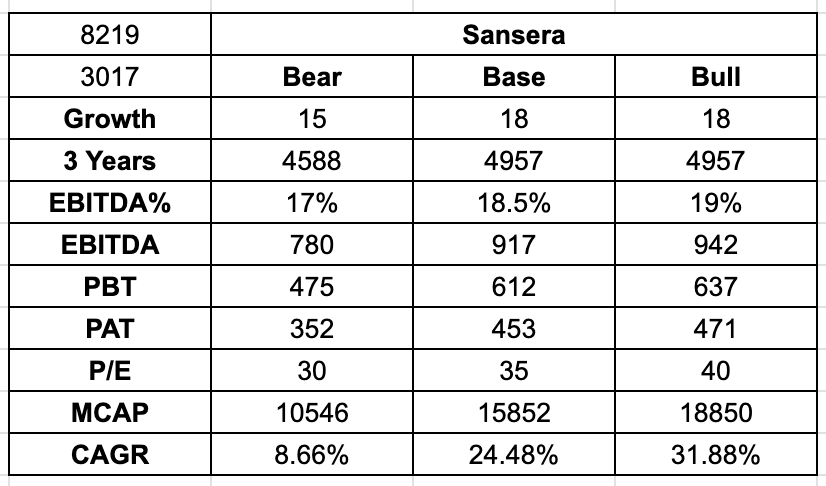

Sansera has the potential to deliver ₹400–450 crore in PAT over the next three years, driven by high-teen revenue growth, margin expansion, and ongoing deleveraging. Businesses with such structural tailwinds—particularly those positioned as precision component suppliers to critical sectors like aerospace, defence, and semiconductors—tend to command premium valuations due to their long-term visibility and terminal value. Sansera fits this narrative well and could be viewed as a structural growth story. While a 20–25% CAGR appears achievable, the inherently lumpy nature of these emerging segments could push the ₹450 crore PAT milestone closer to FY29.

This one looks like a solid long term play