Nintendo: Hidden Gaming Giant

If you grew up playing games, chances are some of your earliest memories involve jumping across platforms with Mario, exploring dungeons with Link, or chasing monsters alongside Pikachu.

For many people, these characters are not just part of video games, they are part of childhood. Entire generations have grown up with worlds like Super Mario Bros., The Legend of Zelda, and Pokémon. The characters persist across decades, passed from one generation of players to the next.

What many investors often forget is that these global cultural icons are owned by a single company: Nintendo.

At first glance, Nintendo appears to be a gaming hardware company. Every few years it launches a new console, such as the Nintendo Switch in 2017 and more recently the Nintendo Switch 2 in 2025.

But the consoles are only part of the story.

Nintendo’s real business is the ecosystem built around its intellectual property. The company sells hardware that brings players into its platform, but the real value comes from the software, games built around beloved franchises like The Legend of Zelda: Breath of the Wild and Animal Crossing: New Horizons, along with digital downloads, subscriptions, and merchandise.

That combination of hardware, software, and iconic characters has created something rare in the gaming industry: a platform sustained not just by technology, but by emotional attachment.

And today, with the launch of the Nintendo Switch 2, Nintendo may be approaching another important inflection point in its earnings power.

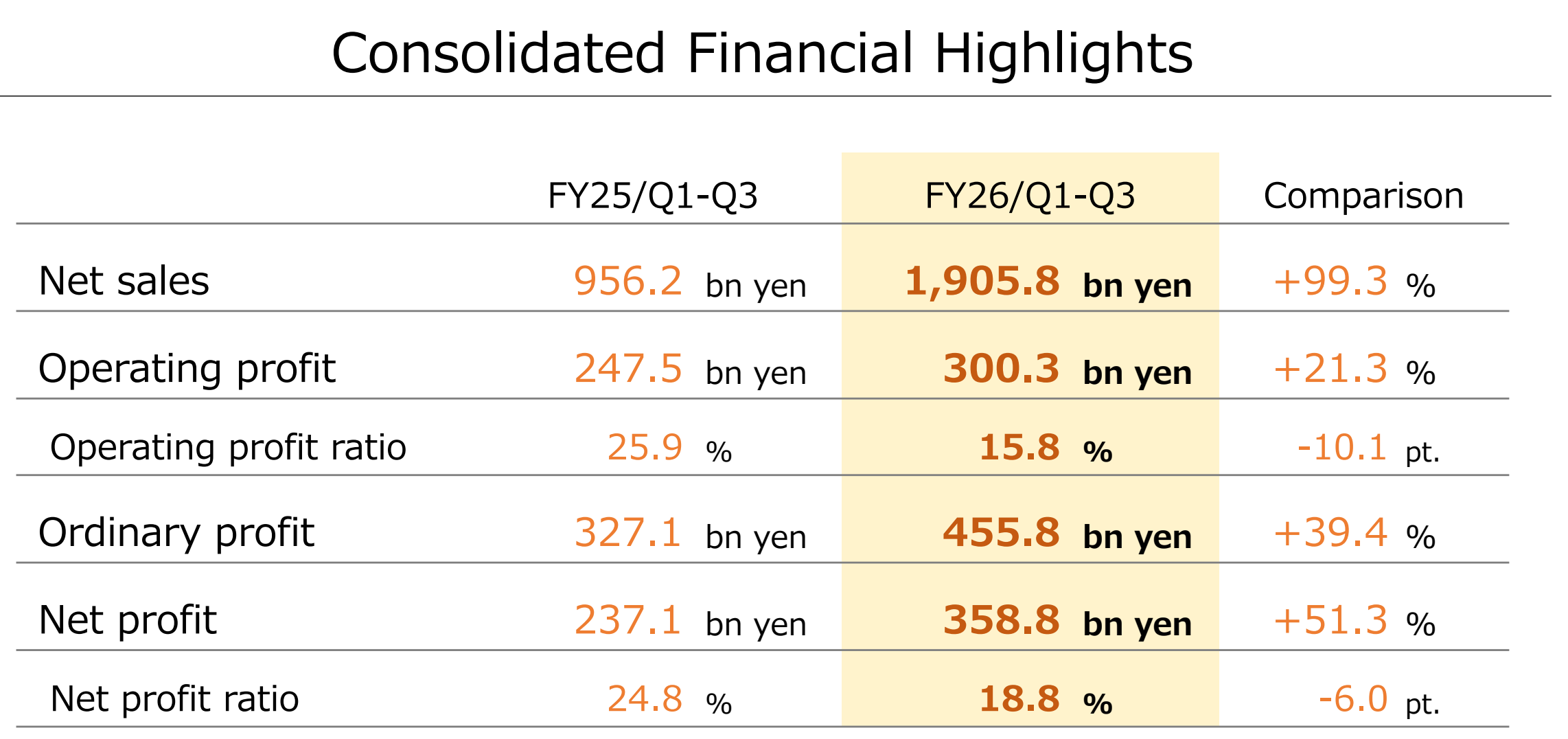

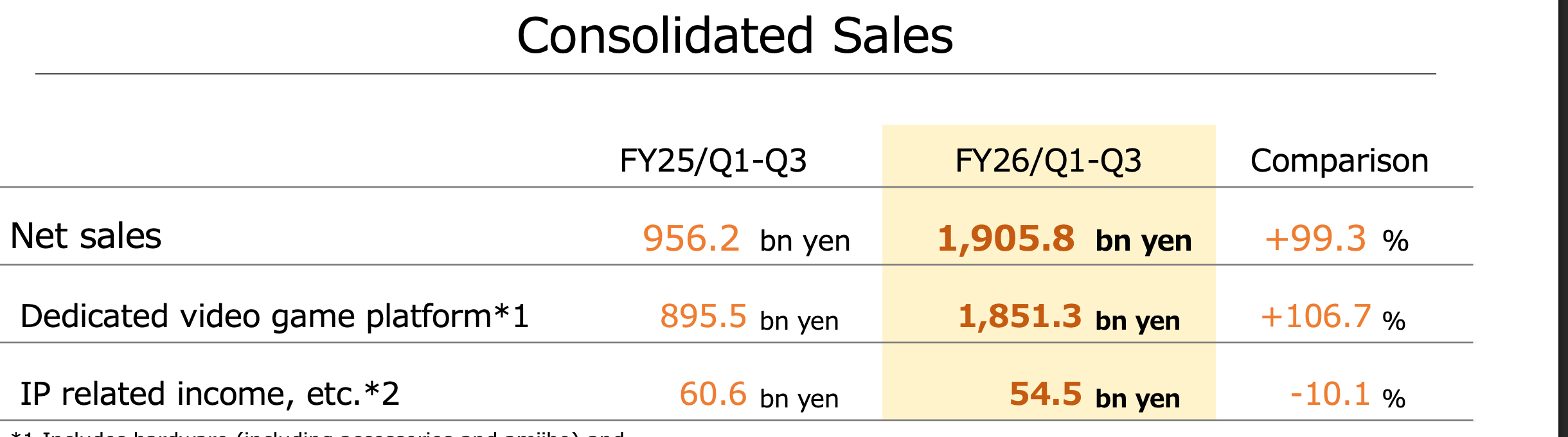

To understand the makeup of the business, Nintendo categorizes its revenue into two primary segments:

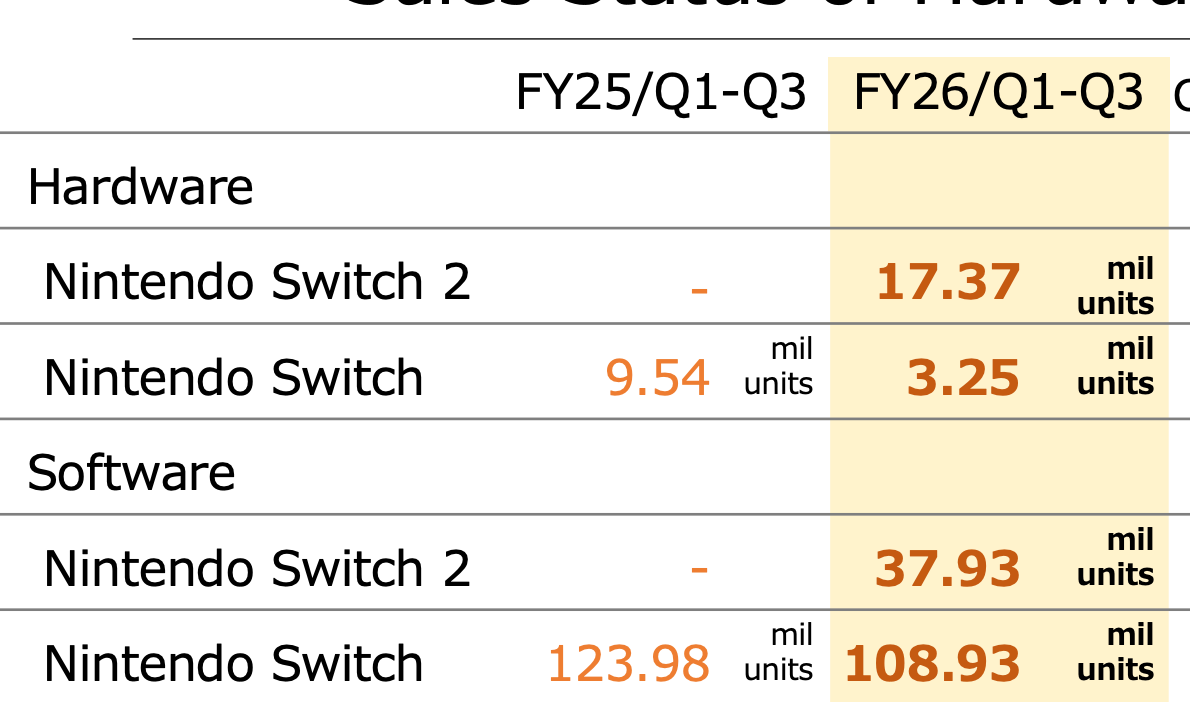

We will look at recent 9MFY26 numbers here:

1. Dedicated Video Game Platform (¥1,851.3 billion)

This is the core engine of Nintendo’s business, making up the vast majority of its revenue. This category blends both the physical hardware consoles and the software ecosystem.

Hardware: This includes the sales of physical consoles and accessories. During this nine-month period, hardware sales were heavily driven by the new console launch, with Nintendo selling 17.37 million Nintendo Switch 2 units and 3.25 million original Nintendo Switch units.

Software: This includes the sale of video games across both systems. Nintendo sold 37.93 million software units for the Switch 2 and 108.93 million software units for the original Switch.

Digital Sales (A Crucial Sub-Segment): Within the broader software category, Nintendo highlights “Digital Sales,” which accounted for 50.4% of total dedicated video game platform software sales. This high-margin category includes:

Downloadable versions of packaged software.

Download-only software.

Add-on content

Recurring subscription revenue from Nintendo Switch Online similar to XBOX Game Pass

2. IP Related Income, etc. (¥54.5 billion)

While a smaller portion of total revenue, this segment represents Nintendo’s efforts to monetize its world-class characters and franchises outside of traditional console gaming. Revenue for this segment was ¥54.5 billion for the nine-month period.

This category includes:

Income from movies and visual content. (Note: Revenue in this segment was down 10.1% year-over-year primarily due to a decrease in movie-related revenue compared to the prior year’s cinematic releases) .

Smart-device (mobile) gaming content.

Licensing royalties.

Merchandise sales at official Nintendo stores.

Thesis

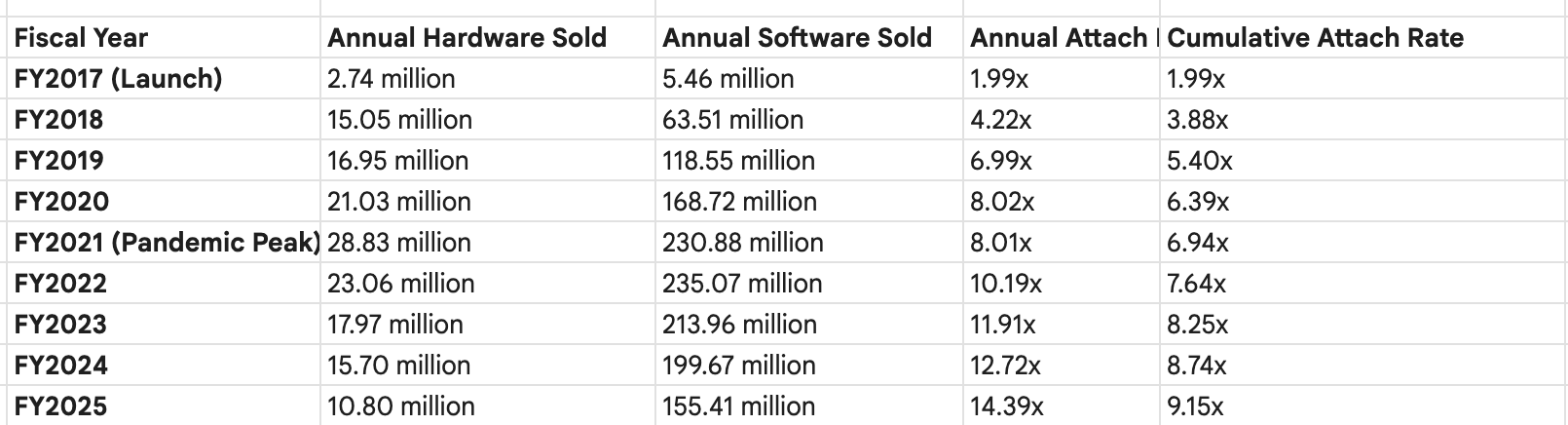

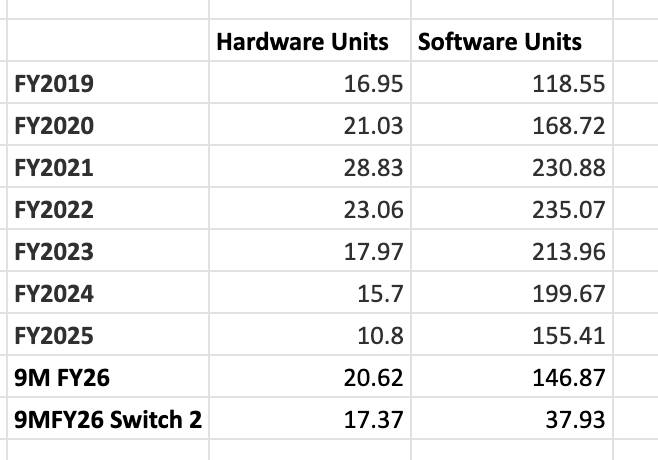

To understand Nintendo’s thesis, lets look at how launch of Nintendo Switch and sale of its software unit sales progressed over the years

Nintendo Switch launched in 2017 and by 2020 it was selling ~170M units of software in a single year.

Fast forward today, Nintendo Switch 2 launched in 2025 has potential to surpass these software unit numbers in 2028/2029. Why can this happen -

Switch 2 can run 3rd party AAA titles

The original Switch’s hardware was too weak to run modern blockbusters natively, so it had to rely almost entirely on Nintendo’s own internal studios to drive software volume.

The original Switch averaged only 3 to 4 major-budget third-party titles per year, and most were older, delayed ports.

The Switch 2 features hardware capable of running current-generation games, resulting in approximately 25 major third-party titles already confirmed for 2026 alone.

This represents a roughly 7x increase in AAA third-party volume compared to any single year of the original Switch, which will dramatically accelerate the overall volume of software sold on the platform.

First Party Games to launch in staggered way

Rather than front-loading all its best games in the launch window of Switch 2 and suffering a mid-generation drought, Nintendo is deliberately back-loading its biggest franchises to ensure sustained momentum across a 5-to-7-year lifecycle.

There are currently 10+ system-selling franchises (each with 20M to 50M unit sales potential) that have not yet debuted on the Switch 2, providing a massive runway for future software velocity.

Better Game Experience

The Switch 2 utilizes Nvidia's DLSS AI technology, which actually upgrades the graphics and frame rates of older original Switch games when played on the new hardware. This incentivizes players to continue buying both new releases and older catalog titles to experience them in higher fidelity.

This is how Nintendo’s hardware units and software units sales progressed over the years.

In FY25, they sold 155M units of Switch compatible software games. In 9MFY26, so far Nintendo has sold 17M+ hardware units of Switch 2 and they would expect to close above 20M+. Next year they can potentially sell 25M units. In next 3 years they might reach 90-100M cumulative hardware unit sales of Switch 2. Given the historical attach rates of software units we can expect Nintendo to be selling 200M units of software units in 3 years for Switch 2 only. Combined with maybe 50-60M units of Switch software they can sell 250M software units in 3 years by FY29.

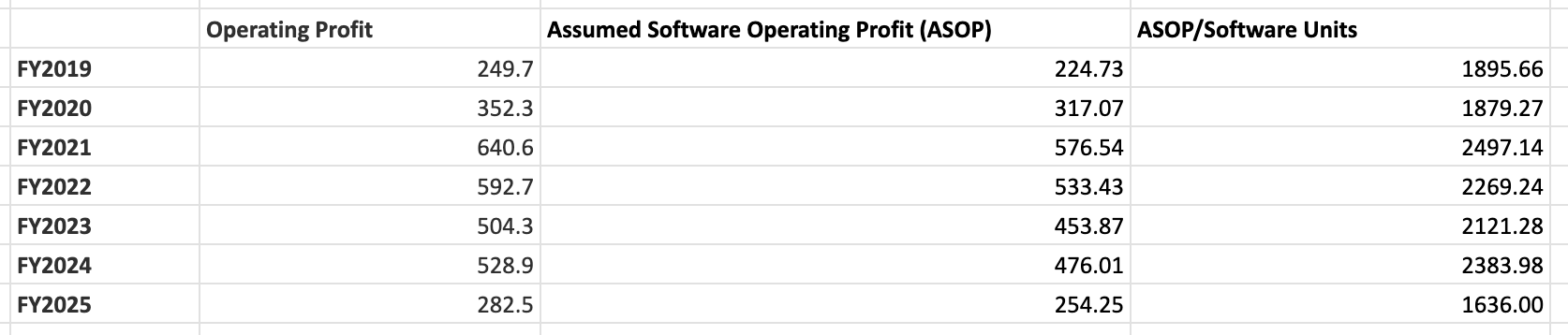

Now, lets estimate operating profit Nintendo can do in 3 years -

This table shows Nintendo’s operating profit over the years (in billion yen). 90% of Nintendo’s profit comes from selling software. More software they sell in a year, more is operating profit margin to overall sales. They have earned upwards of ¥2000 operating profit per software unit sold in past.

So they can earn ¥500-¥550 bn from software sales in FY29.

Now if layer in IP division which is again highly profitable but a smaller sized business and some marginal profits from hardware sales, we are looking at Nintendo doing ¥600 bn of operating profit in 3 years.

Nintendo has several massive IP launches on the immediate horizon that are expected to have a meaningful financial impact:

The Super Mario Galaxy Movie (April 1, 2026): Nintendo is partnering with Illumination again to release this highly anticipated sequel. This movie can act as a massive catalyst to drive software sales on the new Switch 2 console.

A Live-Action Legend of Zelda Movie (2027): Nintendo has officially announced a motion-capture/live-action Zelda film slated for 2027. This project is being developed in partnership with Sony, with the creator of the Marvel Cinematic Universe working alongside Shigeru Miyamoto.

Super Mario’s 40th Anniversary: 2026 marks the 40th anniversary of the Super Mario Bros. franchise. Nintendo’s Q3 FY26 earnings presentation highlights several anniversary initiatives, including new amiibo releases and related merchandise tie-ins. Nintendo may launch a brand-new, mainline 3D Mario game in October 2026 to perfectly capture the cultural momentum of the movie and the anniversary.

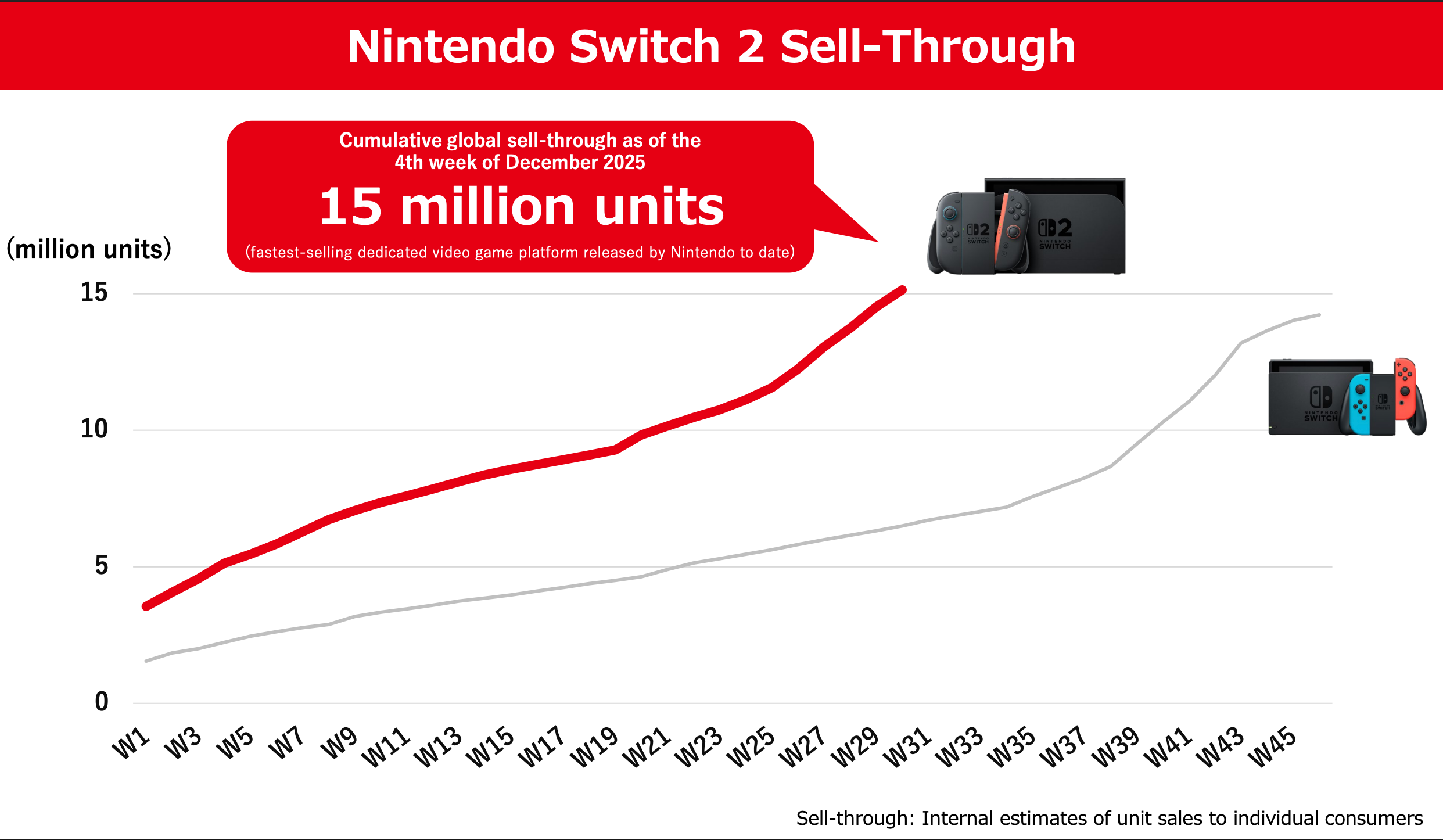

The reason ¥600 bn estimate could prove to be conservative is that it does not take into account much of flow through margins that can happen due to Switch 2 being compatible with 3rd party titles. The original Switch hardware was essentially 2013-era mobile tech, making it too weak to run major AAA third-party games like Call of Duty or Madden. The new Switch 2 (which recently shattered records by selling 3.5 million units in its first four days) features advanced Nvidia architecture. Because it can finally run top-tier third-party blockbusters natively, Nintendo is about to collect an avalanche of new, pure-profit 30% eShop fees on titles it didn’t even have to spend R&D money to develop.

A single Call of Duty game can earn them $15 and on 100M hardware units sold, even 50M units can add up to give them $750M additional free revenue. This $750M translates to ~¥120 bn additional to the profit.

Hence ¥700 bn operating profit is very realistic number for Nintendo. EV/EBIT multiple of 25x multiple is also very realistic given its more of an IP and software led business. This translates to ¥17.5T EV which is ~28-30% IRR.

Now the current stock price decline is mostly due to market being spooked of high RAM costs due to AI boom. RAM is one of the major component in a gaming console. I think it might be constituting 20-25% of hardware COGS and even a 40% jump on this can cause 8% drag on hardware margins. But since majority operating profit are mostly software the effect of this drag can be reduced via 2-3% price increase of console and an another lever of increasing subscription prices for Nintendo Switch Online. Nintendo Switch online is priced much below XBOX and Playstation equivalent membership plans and Nintendo might also pull this lever. Another point to note here is that Nintendo is holding significant inventory and might be able to overcome high pricing for memory atleast in CY26.

The core investment thesis is that the market is currently mispricing Nintendo by applying a “hardware penalty.”

Because investors obsess over temporary hardware margin compression (like rising memory chip costs or US tariffs), Nintendo’s share price is available at a discount. However, this entirely misses the point: hardware margins are essentially irrelevant because software drives the bottom line.

As the Switch 2 installed base expands, projected to hit 20 million units rapidly, the revenue mix will naturally shift back toward high-margin software. Combined with the day-and-date release of AAA third-party games, the sticky NSO subscription revenue, and the self-funding marketing of the NCU, Nintendo’s operating margins (currently hovering in the mid-30s) have a clear pathway to scale further ahead in coming years.

Nintendo shouldn’t be valued as a cyclical toy manufacturer; it deserves the premium multiple of an elite tech platform with a Disney-level IP moat.

Given all this, I think Nintendo is very attractively priced at ¥7.7T Enterprise Value currently and potential to be more than a 2x over next 3 years. By locking users into a permanent, backward-compatible digital ecosystem, the company has insulated itself against the boom-and-bust cycles that used to define its financial statements.

With the hardware power of the Switch 2 unlocking unprecedented third-party platform fees, an expanding cinematic universe acting as a global marketing engine, and an increasingly shareholder-friendly management team, Nintendo is heavily coiled for a breakout. For investors willing to look past short-term noise around component costs, Nintendo represents a generational IP monopoly trading at a noticeable discount to its true platform value.

Disclaimer: This post is for informational purposes only and does not constitute financial advice. Always do your own due diligence.